How to start with £100 — ISAs, ETFs and fees explained, no jargon.

Run a free AI-powered report on any ticker — see how these ideas play out on a real company in under 30 seconds.

In the UK, we're not exactly known for our enthusiasm about the stock market. Not like our American friends, anyway (if I'm still allowed to call them that). Only 26% of UK adults have invested in stocks and shares as of 2025, compared to a whopping 62% of adults in the United States. That's quite the gap. Even Australia significantly outpaces us, with approximately 49% of adults participating in stock markets.

This investment gap extends to newer asset classes too. UK crypto ownership actually dropped to 8% of the adult population in 2025, down from 12% in 2024 according to FCA research. Meanwhile in the US, estimates suggest around 28% of American adults own cryptocurrencies, though other surveys place this figure around 14-21%.

Now, however, we're seeing more of an appetite to invest. With the announced changes to Cash ISAs in the autumn budget, a new wave of investors is emerging. This guide will help you get started with investing. We also recommend going through our investment fundamentals as a next step.

Here's something that might surprise you: if you have a workplace pension, you're probably already invested in the stock market. The thing is, only 36% of people actually know their pension is invested in the stock market. That means nearly two-thirds of pension holders don't realise they already have exposure to equities.

Thanks to auto-enrolment (introduced in 2012), most UK employees now have a workplace pension. As of 2024, around 88% of eligible employees are enrolled in a workplace pension scheme. Your employer contributes, you contribute, and that money gets invested, typically in a diversified mix of shares, bonds, and other assets.

So before you think of yourself as a complete investing novice, it's worth checking what your pension is actually invested in. You might have been building an investment portfolio for years without realising it. Most workplace pensions offer a 'default fund' that's designed to be suitable for most people, but you can often choose different funds if you want more or less risk.

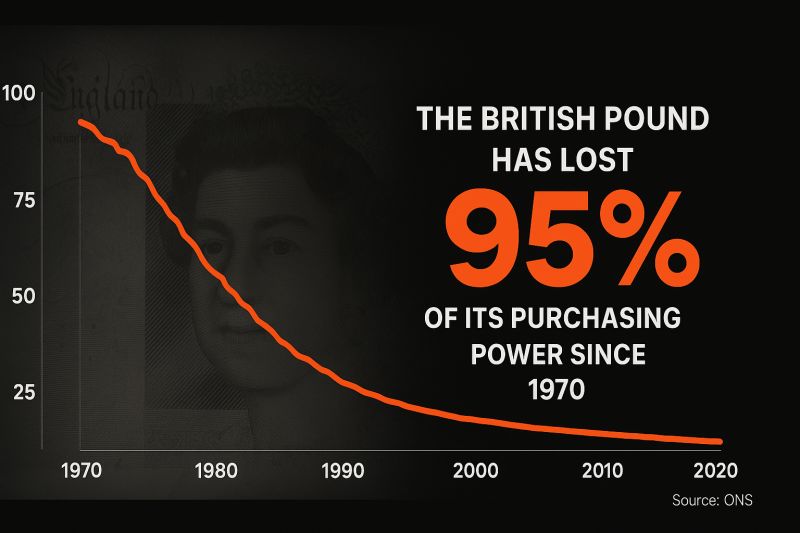

As a nation, we're much more strongly tied to cash and cash-equivalent savings, such as premium bonds. Whilst this form of saving is often seen as low-to-no risk, such an asset has its own hidden costs, notably inflation.

UK inflation rose almost continuously from under 1% in early 2021 to 11.1% in October 2022, a 41-year high, before easing over the following two years. The UK inflation rate for 2022 was 7.92%, while 2023 saw 6.79% and 2024 averaged around 2.5%. As of late 2025, the annual inflation rate in the UK was 3.2%. This means that cash sitting in a standard savings account has been losing purchasing power during most of this period.

This is just the official measure, though. In many ways, purchasing power is much more greatly impacted. Think back ten years. The cost of energy bills and cars have actually surged; a typical household energy bill has jumped from £1,134 to £1,758, while the price of a pint of lager has climbed from £3.48 to roughly £5.50. These aren't just one-off spikes—they represent a sustained yearly inflation of 4–5% on the things people actually spend their money on.

As of November 2025, the average variable cash ISA interest rate is just 1.87%, while the average 1-year fixed-rate ISA offers 4.02%. With inflation at 3.2%, even a fixed-rate ISA barely keeps pace with rising prices, and variable rates mean you're actively losing purchasing power.

Regarding cash holdings, UK households deposited just under £3 billion with banks and building societies in April 2025. As of Q4 2024, UK households managed to save 12% of their income on average, though 1 in 6 adults (16%) across the UK have no savings at all in 2024. That's 8.4 million people.

I also categorise Premium Bonds as a cash saving that falls foul of the same inflationary erosion. Whilst the way interest is paid on premium bonds can feel more exciting (who doesn't love the idea of winning a prize?), statistically they don't perform well.

While the mean return is 3.8% as of April 2025, the median return is lower. For an investor with the maximum £50,000 invested, the median return is 3.3% (£1,650). For investors with lower amounts invested, the median return is lower still. The typical investor with £1,250 or less invested will receive nothing in a year.

Here's a sobering statistic: two-thirds of Premium Bond savers have never won anything. Of the 22.7 million current Premium Bond holders, 14.4 million have never won. That's a lot of people whose money is quietly being eroded by inflation while they wait for a prize that may never come.

Note: What cash savings and premium bonds can be very useful for is your emergency fund, so you have immediate access whilst also earning some interest. More on that later.

In the recent past, rather than the stock markets, the housing market was the outlet for investments for the everyday man or woman with some spare cash. Buying 1-2 additional properties was commonplace from the early 2000s.

The PRS (private rented sector) expanded substantially through the 2000s and early 2010s, more than doubling from 2.1 million homes in 2000 to around 4.8 million by 2015. The expansion was enabled by a low tax, low regulation, and low-interest rate environment, supported by access to credit through buy-to-let mortgages.

Between 2000 and 2008, the outstanding buy-to-let mortgage stock increased from £9 billion to £140 billion, roughly 12% of the overall mortgage market. Property prices also grew significantly: average UK house prices were around £100,000 in 2000, and the average house price is now £270,300 as of November 2025, representing growth of approximately 170% over 25 years.

This was also aided by advantageous tax treatment: before April 2020, landlords could deduct mortgage interest and other allowable costs directly from their rental income, before calculating their tax liability. This system benefited higher and additional rate taxpayers who could claim relief at 40% or 45%. MIRAS (Mortgage Interest Relief at Source) for homeowners was abolished on 6 April 2000.

These changes are forcing people to explore new investment vehicles for their money, which brings us nicely to the stock market.

Before we dive into the practicalities, let's address the elephant in the room: why don't more people invest? Research consistently shows that fear of losing money and the risks associated with investing come out on top as the main reasons people stay away from the stock market.

This fear is entirely understandable. Nobody wants to see their hard-earned money disappear. But here's the thing: by keeping all your money in cash, you're guaranteed to lose purchasing power to inflation. The stock market, while volatile in the short term, has historically grown over longer periods.

For more on these traps, check out our guide on investment psychology.

An important note: everybody's financial goals are different depending on your stage in life, current circumstances, financial position, and end goals. This is important because the decisions you make with investments will and should reflect your state. This is one of the key principles in The Psychology of Money by Morgan Housel, a book we highly recommend.

There are no get-rich-quick schemes, and if someone says there are, they're very likely running some form of scam or, at best, an extremely high-risk investment. Knowing and writing down your long-term goals and starting point is essential.

Interestingly, there's a generational story here. 68% of Gen Z have invested at some point in their lives, the highest percentage across all generations. Younger investors seem to be breaking with the traditional British reluctance to engage with the stock market.

This might be partly driven by the rise of easy-to-use investing apps, the popularity of investment content on social media, and perhaps a recognition that the traditional routes to wealth (like property ownership) are increasingly difficult for younger generations to access.

Okay, so now you should already have a great starting point and a good idea of whether investing in the stock market is right for you.

Luckily in the UK, we have one of the world's best tools for investing: the Stocks and Shares ISA! This provides you with a tax and capital gains-free way of investing up to £20,000 per person. So if you're a couple, that's an amazing £40,000 per year of tax and capital gains-free investing!

The other benefit of ISAs is that you can move funds between cash ISAs and Stocks and Shares ISAs without taking them out of the vehicle. Around 15 million Adult ISA accounts were subscribed to in 2023-24, up from 12.4 million in 2022-23. The share of accounts subscribed to in cash has risen to 66.2%, which suggests there's still plenty of room for more people to discover the benefits of a Stocks and Shares ISA.

ISAs aren't just for funds. A common misconception is that a Stocks and Shares ISA can only hold funds and ETFs. In fact, you can hold individual company shares, ETFs, investment trusts, bonds, and more — all within the same tax-free wrapper. If you later decide to start picking individual stocks alongside your ETFs, your ISA already supports it. For more on combining ETFs and individual stocks, see our ETFs vs Individual Stocks guide.

Now this is the question we get asked the most, and where most people jump to first. The first thing to say is that beating the rate of return for the market is the exception, not the rule. Most professional fund managers don't beat the market consistently over the long term.

Historical returns tell an interesting story:

For most people, investing in a well-diversified ETF (exchange traded fund) is the best way to go, and to continue investing every month without worrying about the specifics. This approach, called 'pound cost averaging', smooths out the ups and downs of the market over time. It also means you don't need the stress of checking the stock market on a frequent basis!

In many cases, you'll also have unique and deep knowledge in a sector that you may not appreciate. Most likely this is either tied to your profession (e.g. you work in accounting and have deep understanding of finance software and companies) or the industry of your company (e.g. you work for a defence firm and have deep understanding of that industry).

These things give you an edge and are your 'circle of competence', as Warren Buffett would say. You may also have company share programmes with discounts. Consider using these first as it gives you an advantage.

For those of you keen to learn and pick individual stocks, we're here to help! Check out our other guides and start using StockRocket to gain deep company understanding.

If you've made it this far, you're already ahead of most people. Understanding why you want to invest, having realistic expectations about returns, and knowing about the tools available to you are the foundations of a successful investment journey.

"The best time to plant a tree was 20 years ago. The second best time is now."

- Chinese Proverb

Happy investing!

Less than you think. Many platforms let you start with as little as £1 through fractional shares, and most have no minimum deposit. The more important question is whether you have your financial foundations in place first: an emergency fund of 3-6 months' expenses, no high-interest debt, and money you won't need for at least 5 years. Once those are sorted, even £25-50 per month into a Stocks and Shares ISA can compound meaningfully over time.

For most beginners, set up a monthly direct debit into a Stocks and Shares ISA and invest in a diversified global ETF like the Vanguard FTSE All-World (VWRL) or a similar low-cost tracker. This gives you instant diversification across thousands of companies, keeps costs minimal, and takes advantage of pound cost averaging. As you learn more and build confidence, you might consider adding individual stocks alongside your ETF foundation.

Yes. A Stocks and Shares ISA can hold individual company shares listed on recognised stock exchanges, as well as ETFs, investment trusts, bonds, and funds. All gains and dividends within the ISA are completely tax-free. This makes it the ideal wrapper for both passive ETF investing and active stock picking.

No. Time in the market matters more than timing the market. Whether the market is at an all-time high or in a dip, history shows that consistent, long-term investing produces strong returns. The S&P 500 has returned roughly 10% annually over nearly a century — through recessions, wars, pandemics, and every kind of crisis. The best time to start was yesterday. The second best time is now.

Disclaimer: This guide is for educational purposes only and does not constitute financial advice. Past performance is not indicative of future results. Always consider seeking advice from a qualified financial advisor before making investment decisions.

Use Stock Rocket AI to get deep, AI-powered analysis of any stock in seconds. Perfect for both beginners and experienced investors.

Deep company research for investors going beyond index funds.

Contact us

chris@stockrocketai.com